How to Avoid PMI Without 20% Down in NY | Integrity Core Realty

Buyer Education · Long Island & Queens

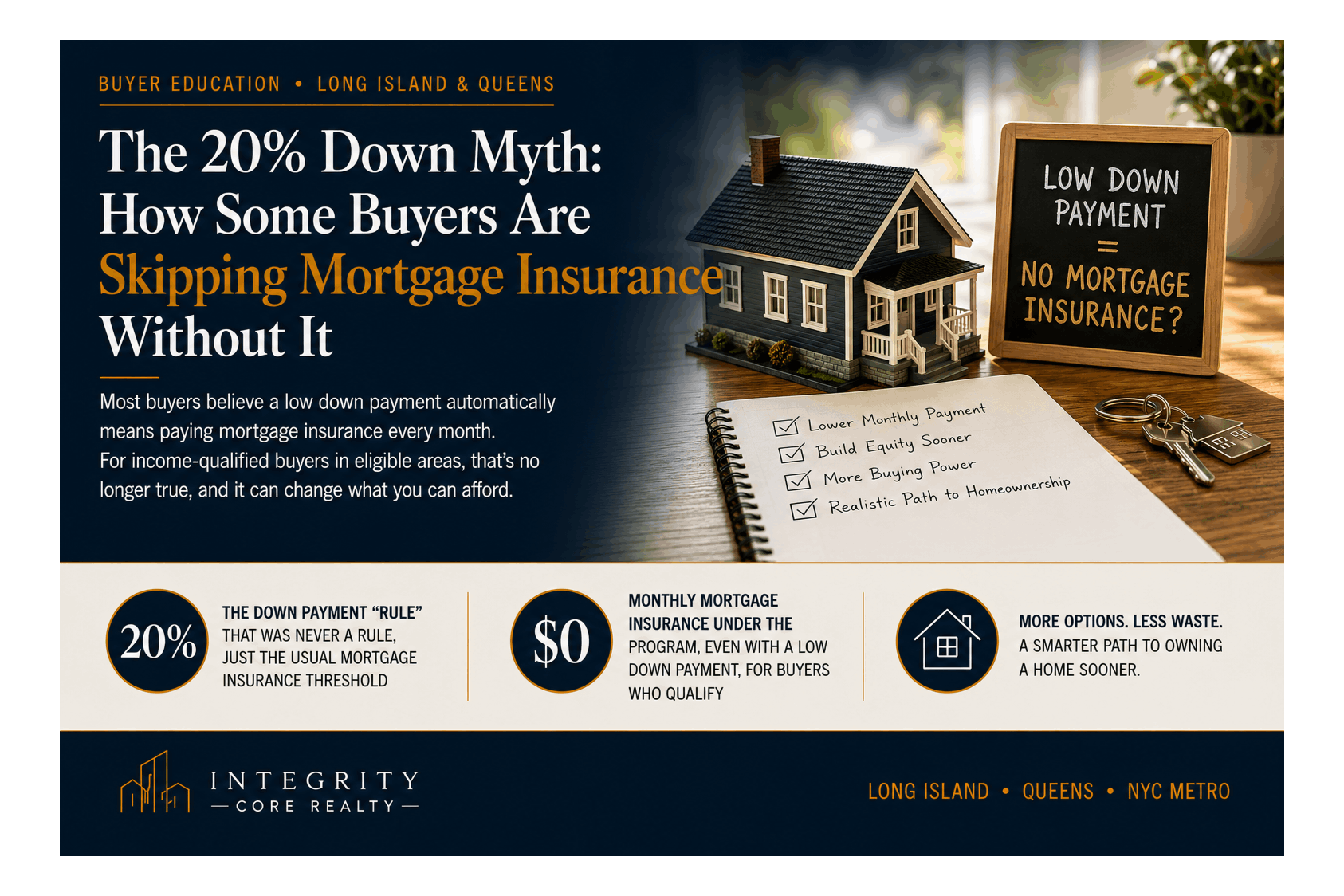

The 20% Down Myth: How Some Buyers Are Skipping Mortgage Insurance Without It

Most buyers believe a low down payment automatically means paying mortgage insurance every month. For income-qualified buyers in eligible areas, that's no longer true, and it can change what you can afford.

Integrity Core Realty | Long Island · Queens · NYC Metro | July 2026 | 6 min read

Ask a room full of renters why they haven't bought a home yet and the answer usually comes down to the same brick wall: the 20 percent down payment. On Long Island and in Queens, where starter homes routinely run $500,000 and up, that means saving six figures before you're even allowed in the game. So people wait. And rents keep climbing while they do.

Here's what most of those renters were never told: 20 percent down has never been a requirement to buy a home. It's the threshold at which lenders stop charging you mortgage insurance. Those are two very different things, and understanding the difference, and the programs built around it, is one of the fastest ways to move your buying timeline up by years.

What Mortgage Insurance Actually Is

When you put down less than 20 percent on a conventional loan, lenders typically require mortgage insurance. Here's the part that stings: you pay for it, but it protects the lender, not you. It's a monthly charge layered on top of your principal, interest, taxes, and homeowners insurance, and depending on your loan size, down payment, and credit profile, it commonly adds anywhere from tens to hundreds of dollars to every monthly payment, money that builds no equity and buys you nothing.

For decades, buyers with smaller down payments simply accepted it as the toll for getting in early. Pay the insurance now, refinance or wait until you hit 20 percent equity, then shed it. That toll is exactly what certain lending programs are now designed to remove.

| 20%The down payment "rule" that was never a rule, just the usual mortgage insurance threshold | $0Monthly mortgage insurance under the program, even with a low down payment, for buyers who qualify | 2Factors that determine eligibility: your total household income and the area you're buying in |

The Program: No Mortgage Insurance, Even With a Low Down Payment

One of our trusted lending partners offers a program built for exactly this problem: it eliminates mortgage insurance entirely, even for buyers putting down well under 20 percent. For qualifying buyers, that means three things at once:

Lower monthly payments. The insurance line item simply isn't there, so more money stays in your pocket every month. Faster equity. More of each payment goes toward the home you own instead of a policy that protects someone else. More buying power. Because your monthly obligation is lower, the same income can qualify you for more house, sometimes the difference between the home you'd settle for and the one you actually want.

Eligibility comes down to two things: your total household income and the location of the home you're buying. The program operates in income-qualified metro and rural areas across eligible counties, and the limits vary by location. The only way to know if you and your target neighborhood qualify is to check, and we do that for you at no cost.

Why We're Telling You This, and How It Works

We're a real estate brokerage, not a mortgage lender. But financing is where most buying journeys quietly stall, so our team stays close to the lending programs that actually move the needle for our clients. When a program like this fits, we make the introduction to our lending partner, they handle the eligibility check and the numbers, and you get answers before you fall in love with a house you're guessing about. You're always free to work with any lender you choose; our job is making sure you know your options.

The process is simple: reach out, tell us your household income range and where you're hoping to buy, and we'll find out whether the program covers you and your target area, usually within a day or two.

Buyer Program Spotlight · Income-Qualified Areas

No Mortgage Insurance. Yes, Even With a Low Down Payment.

Available through our lending partner in income-qualified metro and rural areas across eligible counties. Eligibility is based on your total household income and the area you're purchasing in, and income limits vary by location. One conversation with our team is all it takes to find out if you and your target neighborhood qualify. No cost, no commitment, no pressure.

Integrity Core Realty · (516) 200-1202 · info@icr.homes · We connect you directly with our lending partner

Who Should Check Their Eligibility

Renters who have solid income but haven't stockpiled a 20 percent down payment, which describes most renters on Long Island. First-time buyers who assumed mortgage insurance was simply the price of admission. Buyers who got pre-approved elsewhere and felt squeezed by the monthly number. And anyone shopping in Nassau, Suffolk, or Queens who wants to know whether their target area is income-qualified before they start touring homes. The answer costs nothing and might move your timeline up by years.

"The 20 percent down payment was never the rule. It was just the toll. Some buyers no longer have to pay it."

Related Article

Ready to put that buying power to work? One Suffolk hamlet is mid-comeback, with $100 million in investment reshaping it.

Read: Kings Park, The North Shore Hamlet in the Middle of a $100 Million Comeback →

Frequently Asked Questions

Do you really need 20% down to buy a home?

No. Twenty percent is not a purchase requirement; it's the point at which conventional lenders typically stop requiring mortgage insurance. Many buyers purchase with far less down, and certain programs now remove the mortgage insurance requirement even at low down payments for qualified buyers.

What is PMI and how much does it cost?

Private mortgage insurance is a monthly charge lenders typically require on conventional loans with less than 20 percent down. It protects the lender, not the buyer, and the cost varies with loan size, down payment, and credit profile, commonly adding tens to hundreds of dollars to a monthly payment.

Who qualifies for the no-mortgage-insurance program?

Eligibility is based on two factors: your total household income and the area where you're purchasing. The program operates in income-qualified metro and rural areas within eligible counties, and income limits vary by location. Contact our team and we'll check your specific situation with our lending partner at no cost.

Is Integrity Core Realty a mortgage lender?

No. We are a real estate brokerage. Lending programs, eligibility decisions, rates, and terms come from independent mortgage lenders. We connect our buyers with a trusted lending partner who offers this program, and you are always free to work with any lender you choose.

Does avoiding PMI work with any home?

Under this program, the home's location matters: it must be in an income-qualified metro or rural area within an eligible county. That's why checking eligibility early is so useful, it can help shape where you search before you start touring.

Integrity Core Realty · Guiding Buyers to Smarter Financing

Find Out in One Conversation If You Qualify

Tell us your household income range and where you want to buy. We'll check the program's eligibility map with our lending partner and come back with real answers, then help you find the home to match.

How Integrity Core Realty Can Help You

💔 Divorce Sales 🏚️ Landlord Exit Strategy 🏡 Estate & Probate Sales 📦 Downsizing ⚠️ Pre-Foreclosure Help ✨ Our Story

Disclaimer: Integrity Core Realty is a licensed real estate brokerage, not a mortgage lender or mortgage broker. The lending program described is offered by an independent third-party lender and is subject to that lender's eligibility requirements, income limits, geographic restrictions, underwriting approval, and terms, all of which may change without notice. Nothing in this article is a loan offer, commitment to lend, or guarantee of eligibility, savings, or approval. Program availability varies by location. Buyers are free to work with the lender of their choice. Consult a licensed mortgage professional for details and your own advisors for financial guidance. Integrity Core Realty, 100 Jericho Quadrangle, Suite 235, Jericho, NY 11753. Equal Housing Opportunity.

Categories

- All Blogs (50)

- Affordability (2)

- Buying Tips (6)

- Divorce & Real Estate (5)

- Downsizing & Senior Moves (3)

- Equity (3)

- Expired/Withdrawn/Canceled (1)

- Fairhaven Real Estate Stories (3)

- First-Time Buyers (6)

- For Buyers (24)

- For Sellers (16)

- Forecasts (2)

- Home Prices (2)

- Infographics (1)

- Mortgage Rates (2)

- NY/LI Landlord Resources (6)

- Pre-Foreclosure Options (2)

- Probate & Estate Home Sales (5)

- Rent vs. Buy (2)

- ⚖️ For Attorneys (1)

- 🏡 Featured Listings (14)

- 📍 Local Living (15)

- 📅 Open Houses & Events (2)

- 📊 Real Estate Insights (6)

Recent Posts